Thinking About Selling Your Rental Property?

Read the Article

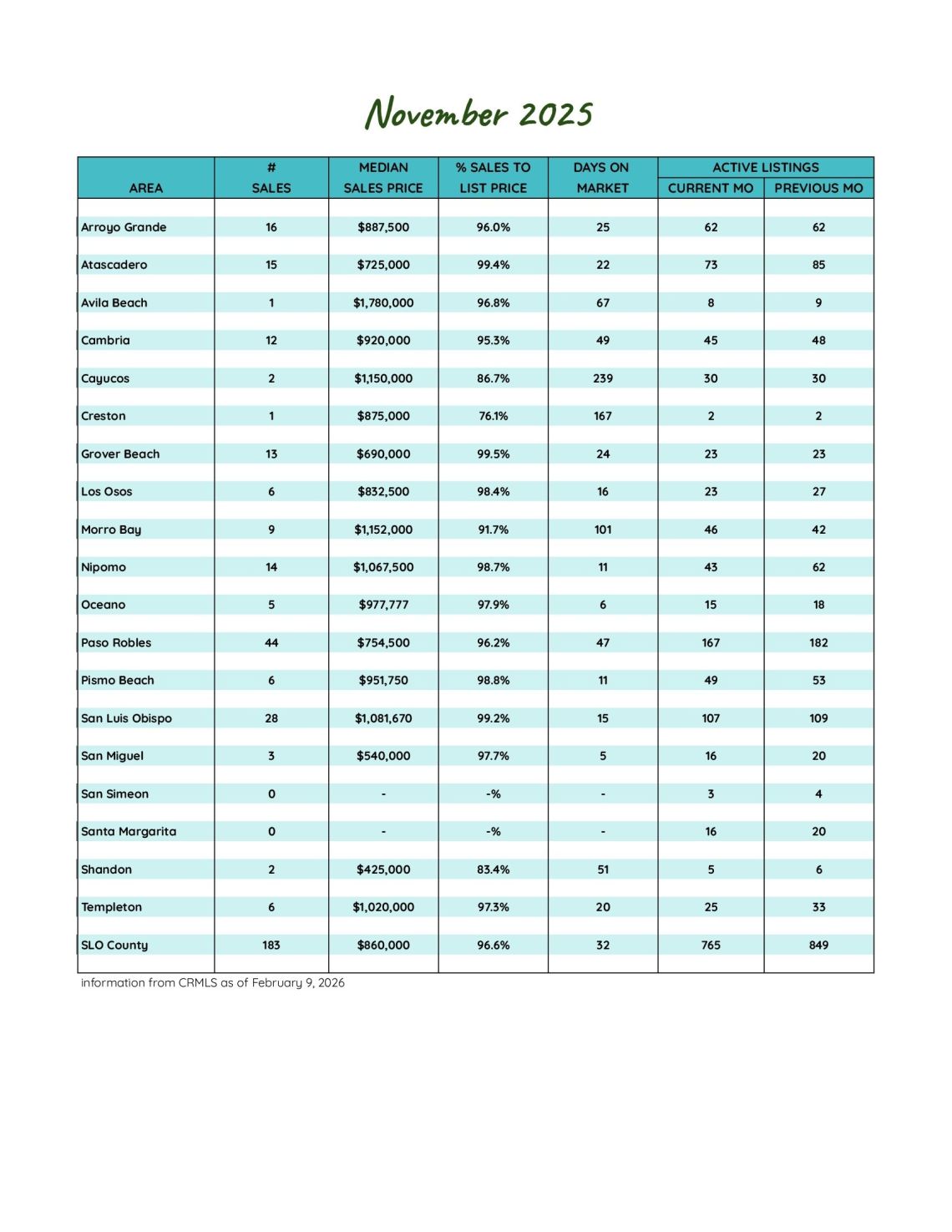

San Luis Obispo County November 2025 Market Update

Seasonal Slowdown Sets In as Prices Hold Steady

As the holiday season approaches, the San Luis Obispo County housing market is easing into its typical late-year slowdown. November’s numbers reflect fewer new listings, moderating buyer activity, and slightly longer market times. Even so, pricing remains steady, and well-positioned homes continue to attract strong interest.

Inventory Trends: Fewer New Listings, Leaner Supply

New listings dropped sharply in November, with 191 homes coming to market—down 33.0% from October’s 285 and 19.1% below November 2024’s 236. Active listings declined to 765, a 9.9% decrease from October’s 849, but still 4.7% higher than a year ago.

The reduction in both new and active inventory reflects typical seasonal pullback. While fewer sellers are entering the market, overall supply remains slightly healthier than last November, maintaining balanced conditions.

Sales Activity: Buyer Momentum Moderates

Pending sales dipped to 188, down 16.4% from October and 5.1% below last year. Closed sales followed a similar pattern, with 183 homes sold—15.7% fewer than October and 6.2% lower than November 2024.

Even as activity slowed, competitive properties continued to move. Thirty-one percent of homes (57 of 183) sold for over asking price, and 31% went under contract within ten days, showing that well-priced homes still generate strong demand.

Pricing and Market Pace: Stable Values, More Negotiation

The average sales price rose to $1,022,011, up 3.5% from October and essentially flat year-over-year. Price per square foot measured $570—down slightly from October but up 3.4% compared to last November, indicating continued long-term value stability.

Homes averaged 51 days on market, compared to 47 in October and 41 a year ago, suggesting buyers are taking more time and negotiating more strategically. The list-to-sale price ratio softened to 94.9%, down from 95.8% in October and 96.6% last year.

Months of supply registered at 3.5, down from 3.9 in October and just slightly above last year’s 3.4—still indicative of balanced conditions rather than a buyer’s market.

Luxury and Community Highlights

Luxury activity remained strong. Six communities recorded average sales prices above $1,000,000, while three communities remained under $750,000, offering entry-level opportunities across the county. Eleven properties sold for over $2,000,000, including a Paso Robles estate that topped $5,500,000. The upper end of the market continues to demonstrate resilience even as overall pace slows.

What It Means for Buyers and Sellers

For sellers, November reinforces the importance of strategic pricing and thoughtful presentation. While strong homes are still commanding premium offers, buyers have more time and leverage than in recent years. For buyers, increased inventory compared to last fall provides greater choice and negotiating room—though desirable homes are still moving quickly.

As we head into winter, the market appears stable and balanced: less frenzied than peak seasons, but far from stagnant. The fundamentals remain solid, with steady pricing and consistent demand across price ranges.

191

New Listings

2024: 236

765

Active Listings

2024: 731

188

Under Contract

2024: 198

183

Closed Sales

2024: 195

Homes Sold

94.9%

Sale-to-List Price

2024: 96.6%

$1,022,011

Avg Sales Price

2024: $1,020,982

3.5

Months of Supply

2024: 3.4

51

Avg Days on Market

2024: 41

$570

Avg Price per Sq Foot

2024: $551